RBSE Solutions for Class 11 Accountancy Chapter 7 Depreciation, Provisions and Reserves

Rajasthan Board RBSE Solutions for Class 11 Accountancy Chapter 7 Depreciation, Provisions and Reserves Textbook Exercise Questions and Answers.

Rajasthan Board RBSE Solutions for Class 11 Accountancy in Hindi Medium & English Medium are part of RBSE Solutions for Class 11. Students can also read RBSE Class 11 Accountancy Important Questions for exam preparation. Students can also go through RBSE Class 11 Accountancy Notes to understand and remember the concepts easily.

RBSE Class 11 Accountancy Solutions Chapter 7 Depreciation, Provisions and Reserves

RBSE Class 11 Accountancy Depreciation, Provisions and Reserves Textbook Questions and Answers

Test Your Understanding I

1. You are looking at the profit and loss account of three business enterprises. You find the term depletion in first case and amortisation in third case. State the type of business of two enterprises are into.

2. A pharmaceutical manufacturer has just developed and registered a patent for a rare medicine. Which term will appear in its profit and loss account regarding the cost of patent written-off.

Answers:

1. Fixed assets, exhaustion of natural resources, specific contracted business.

2. Amortisation.

Test Your Understanding II

State whether the following statements are true or false:

1. Depreciation is a non-cash expense.

2. Depreciation is also charged on current assets.

3. Depreciation is decline in the market value of tangible fixed assets.

4. The main cause of depreciation is wear and tear caused by its usage.

5. Depreciation must be charged so as to ascertain true profit or loss of the business.

6. Depletion term is used in case of intangible assets.

7. Depreciation provides fund for replacement.

8. When market value of an asset is higher than book value, depreciation is not charged.

9. Depreciation is charged to reduce the value of asset to its market value.

10. If adequate maintenance expenditure is incurred, depreciation need not be charged.

Answers:

1. (True)

2. (False)

3. (False)

4. (True)

5. (True)

6. (False)

7. (True)

8. (False)

9. (False)

10. (False)

Test Your Understanding III

1. There are two dentists Dr. Aggarwal and Dr. Mehta in your locality who are competitors. Both of them have recently bought an equipment for treatment of patients. Dr. Aggarwal has decided to write-off an equal amount of depreciation every year while Dr. Mehta wants to write-off a larger amount in earlier years. They do not know anything about the methods of depreciation. Who is wise in your opinion? Give reasons in support of your answer.

Answer:

Written down value method is more appropriate because this method is suitable for those assets which are affected by technological changes. Moreover, this method is recognised by income tax. According to our opinion, Dr. Mehta is more wise in his opinion because assets are used maximum in the beginning of its life.

Test Your Understanding IV

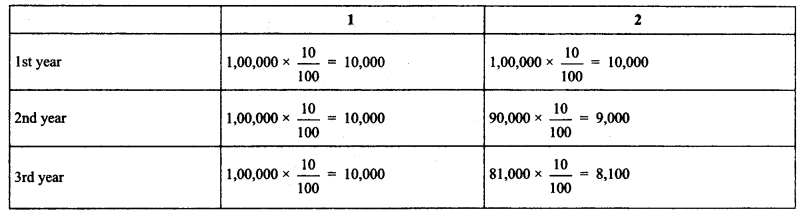

Basaria Confectioner bought a cold storage plant on July 01,2014 for ₹ 1,00,000.

Compare the amount of depreciation charged for first three years using:

1. Rate of depreciation @ 10% on original cost basis;

2. Rate of depreciation @ on written down value basis;

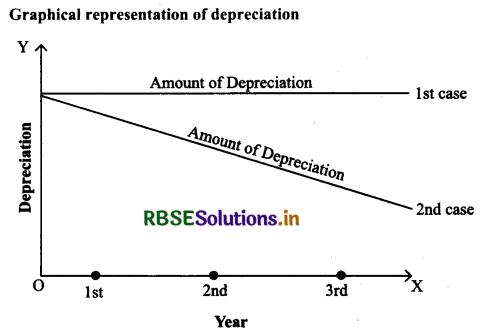

3. Also, plot the computed amount of depreciation on a graph.

Suggested answer: Calculation of depreciation in both cases

By comparing amount of depreciation, in both cases, we conclude that amount of depreciation will be constant in each year and book value of plant will be zero but there shall be some salvage value. While in 2nd case amount of depreciation is decreasing year by year and value of plant will never be zero which is true.

Test Your Understanding V

I. State with reasons whether the following statements are True or False:

(i) Making excessive provision for doubtful debits builds up the secret reserve in the business.

(ii) Capital reserves are normally created out of free or distributable profits.

(iii) Dividend equalisation reserve is an example of general reserve.

(iv) General reserve can be used only for some specific purposes.

(v) ‘Provision’ is a charge against profit.

(vi) Reserves are created to meet future expenses or losses the amount of which is not certain.

(vii) Creation of reserve reduces taxable profits of the business.

Answers:

(i) True, because actual bad debts will be less than the provision and unutilised provision becomes secret reserve in the business.

(ii) False, because capital reserves are created out of capital profits only.

(iii) False, because it is an example of specific reserve.

(iv) False, because general reserve is created without any specific reason. Hence, this can be used as per the requirement of business.

(v) True, because ‘Provision’ reduces the amount of net profits.

(vi) False, because reserves are created for uncertainties of future which are unknown.

(vii) False, reserves reduces only divisible profit. Hence, tax cannot be reduced by creating reserves.

II. Fill in the correct words:

(i) Depreciation is decline in the value of ......................

(ii) Installation, freight and transport expenses are a part of ......................

(iii) Provision is a ...................... against profit.

(iv) Reserve created for maintaining a stable rate of dividend is termed as ......................

Answers:

(i) Fixed Assets

(ii) Acquisition cost

(iii) Charge

(iv) Dividend equilisation reserve.

Short Answer type Questions

Question 1.

What is ‘Depreciation’?

Answer:

Depreciation described as a permanent, continuing and gradual shrinkage in the book value of fixed assets due to the use, passage of time and obsolescence through technology or market change.

Question 2.

State briefly the need for providing depreciation.

Answer:

Need of Charging Depreciation:

(a) To Ascertain the [rue Result of the Business: To arrive at the true profits, depreciation must be provided for and recorded as a loss of the business.

(b) To Replace an Asset: To replace certain assets which become useless after sometime by the new ones, a provision of depreciation should be made by setting aside every year an amount equal to the depreciation of an assets.

(c) To Exhibit True Value of Balance Sheet: It is not possible to show assets at their true values in a Balance Sheet unless depreciation is deducted from their values.

(d) To Spread the loss Caused Depreciation of Assets Over a Number of Years: The loss in the value of assets is undoubtedly a loss of the business and it is spread over a number of years by making a provision for depreciation.

(e) To Make Correct Payment of Income Tax: If no provision for depreciation is made the profit of the year will enhance and due profit more income tax will have to be paid.

Question 3.

What are the causes of depreciation?

Answer:

Meaning: Depreciation described as a permanent, continuing and gradual shrinkage in the book value of fixed assets due to the use, passage of time and obsolescence through technology or market change. It is the expired cost of fixed asset which is charged against the revenue of a given period.

Features of Depreciation:

(a) Depreciation is the fall in the value of fixed assets. These assets include machines, plants, furniture, buildings, computers,trucks, vans, equipments, etc.

(b) It is an expired cost of the fixed asset.

(c) It is a non-cash expense.

(d) Deprecation is a continuous, regular, gradual and permanent decline in the book value of an asset.

(e) Depreciation is not always physical deterioration but loss of usefulness from business point of view.

(J) Depreciation charged on tangible fixed assets (also known as depreciable asset). The term is not used for fictitious assets such as goodwill, patent right, etc. and wastmg assets such as mines.

Question 4.

Explain basic factors affecting the amount of depreciation.

Answer:

Amount of charging depreciation depends upon three factors:

(a) Cost of Asset: It is also known as historical cost or original cost. It includes cost price and other costs which are incurred to put the asset into working condition. All such costs are capital in nature and once the asset comes into working capital, the expenses which are incurred to keep the asset into running condition, are considered as revenue expenditure. All revenue expenditures are shown in the profit and loss account.

Cost of asset = Cost price + all cost incurred from the date of purchase till asset is put to use.

Costs other than cost price = Freight, transportation, transit insurance, installation cost, registration cost, commission on purchase, initial repairs, softwares for asset bought.

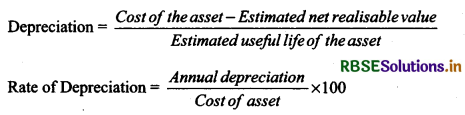

(b) Estimated Net Residual Value: It is also known as the salvage value or scrap value which is estimated to be realised after the end of its useful life. Such value is reduced by the associated cost necessary to incur.

Depreciable Cost: It is the cost which is the base to find out the amount of depreciation. It is calculated by deducing

residual value of asset from the cost of the asset.

Depreciation cost = Cos of the Asset - Net Realisable value.

(c) Estimated Useful Life: Useful life of an asset is economic or commercial life of the asset. Physically life is not important as asset may exist but it may not be commercially viable due to outdated technology or its effectiveness to produce as desired.

Question 5.

Distinguish between straight line method and written down value method of calculating depreciation.

Answer:

|

Basis |

Straight line method |

Written down value method |

|

1. Basis |

It is calculated on the original cost of asset every year |

It is calculated on the original cost in the first year and on the book value thereafter. |

|

2. Amount of depreciation |

The yearly amount of depreciation remains same every year |

The amount of depreciation goes on decreasing every year. |

|

3. Burden of depreciation |

It creates more burden on the profits in later years. |

As the book value of asset decreases, the amount of depreciation decreases and balanced burden on profits every year. |

|

4. Book value on the expiry of life |

Book value becomes zero at the end of estimated life of asset |

The book value never becomes zero. |

|

5. Recognition as per law |

It is not recognized under Income Tax Law |

It is recognized under income tax law. |

Question 6.

“In case of a long term asset, repair and maintenance expenses are expected to rise in later years than in earlier year”. Which method is suitable for charging depreciation if the management does not want to increase burden on profits and loss account on account of depreciation and repair.

Answer:

Written down value method is most appropriate as in the initial years, high amount of depreciation is provided which reduces the burden of repair and maintenance in the later years.

Question 7.

What are the effects of depreciation on profit and loss account and balance sheet?

Answer:

Effects of depreciation on profit and loss account:

(1) Depreciation is shown on the debit side of profit and loss account which reduces the net profit.

(2) It reduces the tax liability

Effects of depreciation on balance sheet

(1) The depreciation reduces the value of fixed asset.

(2) Either reduced value of fixed asset is shown or original cost is shown on the asset side and its accumulated depreciation is shown as a deduction from the asset or on the liabilities side.

Question 8.

Distinguish between ‘provision’ and ‘reserve’.

Answer:

|

Basis |

Provision |

Reserve |

|

1. Nature

|

It is charge against the profit |

It is an appropriation in nature |

|

2. Purpose

|

It is created for a known liability |

It is created to strengthen the financial position |

|

3. Effect on taxable income

|

It reduces taxable income |

It does not affect taxable income as it is created out of taxed income |

|

4. Presentation

|

It is shown as deduction from the asset concerned or on the liabilities side |

It is always shown on the liabilities side under reserves and surplus |

Question 9.

Give four examples each of ‘provision’ and ‘reserves’.

Answer:

Examples of Provisions:

(1) Provision for Depreciation, Repairs and Renewals of assets.

(2) Provision for Taxation.

(3) Provision for Bad and Doubtful Debts.

(4) Provision for Discount on Debtors.

(5) Provision for Fluctuations in the value of Investments.

Examples of reserves:

1. General Reserve.

2. Capital Reserve.

3. Debenture Redemption Reserve.

4. Dividend Equalization Reserve.

5. Workman Compensation Reserve.

Question 10.

Distinguish between ‘revenue reserve’ and ‘capital reserve’.

Answer:

Difference between revenue reserve and capital reserve

|

Basis |

Revenue reserve |

Capital reserve |

|

1. Source of creation |

These are created out of profit and loss |

These are created out of capital profits |

|

2. Usage |

These reserves can be used to pay a dividend |

These reserves cannot be used to give dividends |

|

3. Purpose |

These are created to meet unforeseen losses. |

These are created to write off capital losses. |

Question 11

Give four examples each of ‘revenue reserve’ and ‘capital reserves’.

Answer:

Examples of reserves:

|

Revenue reserves |

Capital reserves |

|

Profit on sale of fixed Assets Capital Redemption Reserve Profit on Revaluation of Fixed Assets & Liabilities. Profit prior to incorporation. |

Question 12.

Distinguish between ‘general reserve’ and ‘specific reserve’.

Answer:

General Reserve: This is a reserve which is created out of profits. General reserve is created to strengthen the financial position of the company and can be used to meet contingencies, increasing the working capital, maintaining the same rate of dividend as declared in the past years.

Specific Reserves: Specific reserve represents a sum charged against profits to provide for a known contingency. If it is meant for a specific purpose, it is called specific reserve. Reserve for doubtful debts, depreciation etc. are the specific reserves.

Question 13.

Explain the concept of ‘secret reserve’.

Answer:

Meaning: Retaining a part of profit not for any particular expense, loss and liability but to strengthen the financial position or to meet financial needs of future, is called reserve. It is an appropriation of profit, means it is created if the profits are available. When a reserves is created, it reduces the availability of profits to the owners and in case of companies, shareholders receive lower amount of dividend.

ExampIes: General reserve, Workmen compensation reserve, Investment fluctuation fund, Capital reserve, Dividend equalisation reserve, Reserve for redemption of debenture etc.

Long Answer type Questions

Question 1.

Explain the concept of depreciation. What is the need for charging depreciation and what are the causes of depreciation?

Answer:

Meaning: Depreciation described as a permanent, continuing and gradual shrinkage in the book value of fixed assets due to the use, passage of time and obsolescence through technology or market change. It is the expired cost of fixed asset which is charged against the revenue of a given period.

Features of Depreciation:

(a) Depreciation is the fall in the value of fixed assets. These assets include machines, plants, furniture, buildings, computers, trucks, vans, equipments, etc.

(b) It is an expired cost of the fixed asset.

(c) It is a non-cash expense.

(d) Deprecation is a continuous, regular, gradual and permanent decline in the book value of an asset.

(e) Depreciation is not always physical deterioration but loss of usefulness from business point of view.

(f) Depreciation charged on tangible fixed assets (also known as depreciable asset). The term is not used for fictitious assets

such as goodwill, patent right, etc. and wasting assets such as mines.

Need of Charging Depreciation:

(a) To Ascertain the True Result of the Business: To arrive at the true profits, depreciation must be provided for and recorded as a loss of the business.

(b) To Replace an Asset: To replace certain assets which become useless after sometime by the new ones, a provision of depreciation should be made by setting aside every year an amount equal to the depreciation of an assets.

(c) To Exhibit True Value of Balance Sheet: it is not possible to show assets at their true values in a Balance Sheet unless depreciation is deducted from their values.

(d) To Spread the loss Caused depreciation of Assets over number of year: The loss in the value of assets is undoubtedly a loss of the business and it is spread over a number of years by making a provision for depreciation.

(e) To lake Correct Payment of Income Tax: If no provision for depreciation is made the profit of the year will enhance and due profit more income tax will have to be paid.

Question 2.

Discuss in detail the straight line method and written down value method of depreciation. Distinguish between the two and also give situations where they are useful.

Answer:

There are two methods mandated by law and enforced by professional accounting practice. These are:

(a) Straight Line Method: This method is also known as fixed instalment method or original cost method. Fixed amount of depreciation is charged on the basis of usage in an accounting year and the cost is reduced to its salvage value.

Advantages of Straight Line Method

(a) Simple to use and popular

(b) Possible to distribute full depreciable cost over useful life to scrap value or ml.

(c) Makes comparison of profits easy as same amount of depreciation is used every year.

Limitations of Straight Line Method

(a) Faulty assumption of same amount of the utility of an asset in different accounting years.

(b) Total amount charged on account of depreciation and repairs taken together do not remain uniform throughout the life of the asset.

(c) It does not take effective use of asset.

Suitability: It is suitable where the useful life of the asset can be estimated accurately such as leasehold building, patents etc. where the repair charges are low and possibility of obsolescence is low.

(b) Written down value method: It is also known as diminishing balance method and reducing balance method. At the every year, depreciation is charged on the book value of the asset. This method is based on the assumption that benefit from the asset goes on decreasing with the passage of time and hence amount of depreciation goes on decreasing each year.

Calculation of Depreciation: Depreciation is calculated at a fixed percentage on the original cost in the first year but in subsequent years it is calculated at the same percentage on the written down value gradually reducing during the expected working life of the asset.

Question 3.

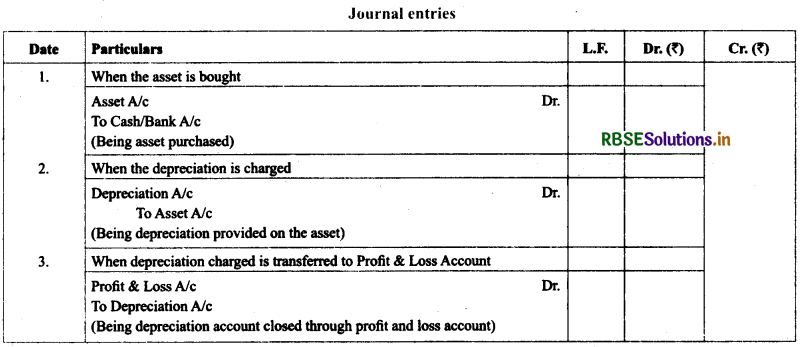

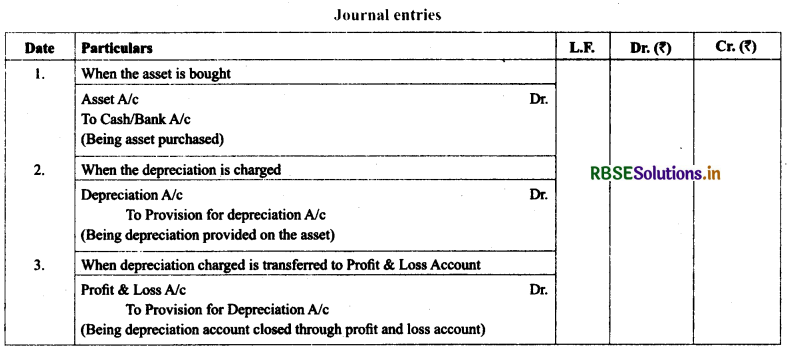

Describe in detail two methods of recording depreciation. Also give the necessary journal entries.

Answer:

There are two methods of recording depreciation:

(a) When the depreciation is Charged to the Asset Concerned

Under this method, depreciation is charged on the cost of the asset at the end of each year and the same is subtracted from its value on the asset side of the balance sheet.

(b) When the Depreciation Fund is Maintained for the Asset Concerned

Under this method, asset account is maintained at its original cost and depreciation required on such assets is recorded in a separate account meant for this purpose, it is known as ‘Provision for depreciation’ or Accumulated depreciation A/c’ or Accumulated depreciation A/c’.

Provision for depreciation continue to increase every year and it is transferred to the asset account when the asset is discarded or sold. It is transferred to asset account wholly if the whole asset is sold/discarded or proportionately if a part of the asset is sold/discarded.

Question 4.

Explain determinants of the amount of depreciation.

Answer:

Factors Affecting the Amount of Depreciation

Amount of charging depreciation depends upon three factors:

(i) Cost of Asset: It is also known as historical cost or original cost. It includes cost price and other costs which are

incurred to put the asset into working condition. All such costs are capital in nature and once the asset comes into

working capital, the expenses which are incurred to keep the asset into running condition, are considered as revenue

expenditure. All revenue expenditures are shown in the profit and loss account.

Cost of asset = Cost price + all cost incurred from the date of purchase till asset is put to use.

Costs other than cost price = Freight, transportation, transit insurance, installation cost, registration cost, commission

on purchase, initial repairs, softwares for asset bought.

(b) Esilmaled Net Residual Value: It is also known as the salvage value or scrap value which is estimated to be realised

after the end of its useful life. Such value is reduced by the associated cost necessary to incur.

Depreciable Cost: It is the cost which is the base to find out the amount of depreciation. It is calculated by deducing

residual value of asset from the cost of the asset.

Depreciation cost = Cost of the Asset — Net Realisable value.

(c) Estimated Useful Life: Useful life of an asset is economic or commercial life of the asset. Physically life is not

important as asset may exist but it may not be commercially viable due to outdated technology or its effectiveness to

produce as desired.

Question 5.

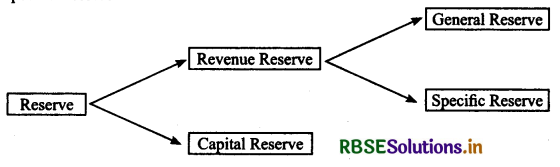

Name and explain different types of reserves in details.

Answer:

Meaning: Retaining a part of profit not for any particular expense, loss and liability but to strengthen the financial position or

to meet financial needs of future, is called reserve. It is an appropriation of profit, means it is created if the profits are available. When a reserves is created, it reduces the availability of profits to the owners and in case of companies, shareholders receive lower amount of dividend.

EarnpIes: General reserve, Workmen compensation reserve, Investment fluctuation fund, Capital reserve, Dividend equalisation reserve, Reserve for redemption of debenture etc.

Types of Reserves:

Reserve can be broadly classified as Revenue Reserve and Capital Reserve

General Reserve and Specific Reserve:

(A) Revenue Reserve: These are the reserve which are created out of divisible profits which would have been distributed as profit among owner(s) or shareholders. Revenue reserve may be classified into two categories:

(a) General Reserve: When a reserve is created without any purpose, it is called as general reserve. It is meant for future emergencies or expansion of the business. It is a free reserve and management can utilise for any purpose.

(b) Specific Reserve : It is a reserve which is created for some specific purpose and it can be used only for such purpose for which it is created.

Some of the specific reserves are:

(1) Dividend Equilisation Reserve: It is maintained to stabalise the dividend rate. It is used to declare dividend in the year of low profits or no profits.

(2) Workmen Compensation Reserve: It is created to write off the various claims settled between management and employees.

(3) Investment Fluctuation Fund: It is created to set off the decline in the value of investments.

(4) Debenture Redemption Reserved is created under legal norms to repay the amount of debentures outstanding in time.

(B) Capital Reserve: These reserve are created due to occurring of capital profits. These do not arise from the normal operating activities. These reserves are not available for the distribution as dividend but are used to write off capital expenditures and losses etc.

Example of such reserves are:

(1) Premium on issue of shares or debenture.

(2) Profit on sale of fixed assets.

(3) Profit on redemption of debentures.

(4) Profit on revaluation of fixed asset & liabilities.

(5) Profits prior to incorporation.

(6) Profit on reissue of forfeited shares

Question 6.

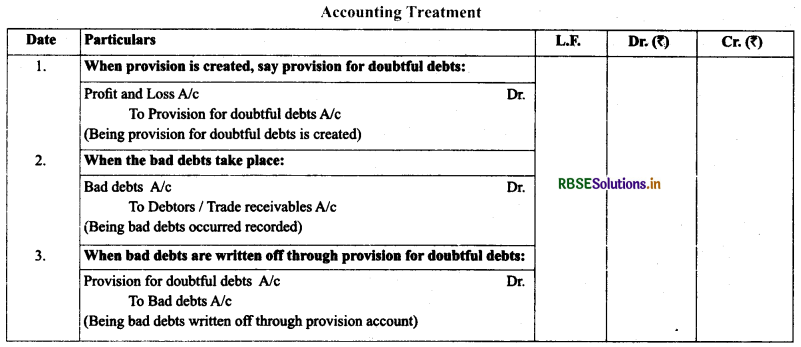

What are ‘provisions’? How are they created? Give accounting treatment in case of provision for doubtful Debts.

Answer:

Meaning: Retaining a part of profit for an expense or loss for which amount is not certain is called provision. It is charged against the profit, means it is created even a firm involves loss and is shown on the debt side of profit and loss account while creating.

Examples: Provision for depreciation, Provision for bad and doubtful debts, Provision for taxation, Provision for discount on debtors, and Provision for repairs and renewals.

Disclosure: The provisions which have been against the use of any asset, are shown as deduction from their respective assets on the assets side and others are shown on the liabilities side.

Numerical Questions

Question 1.

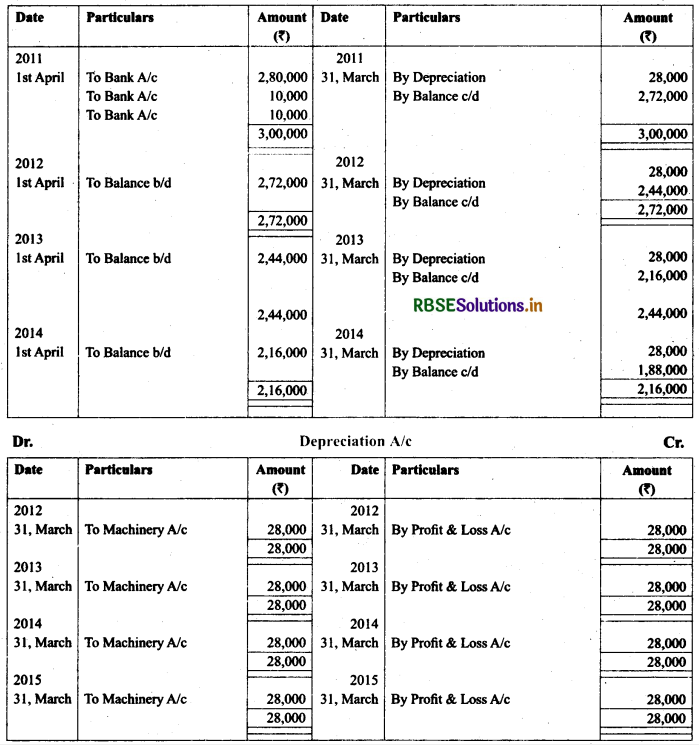

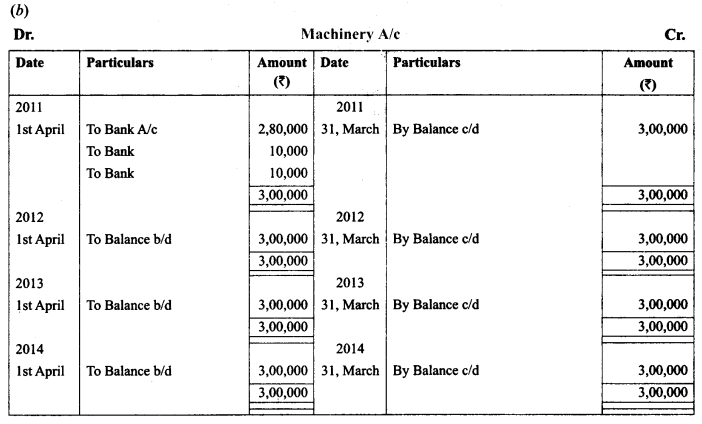

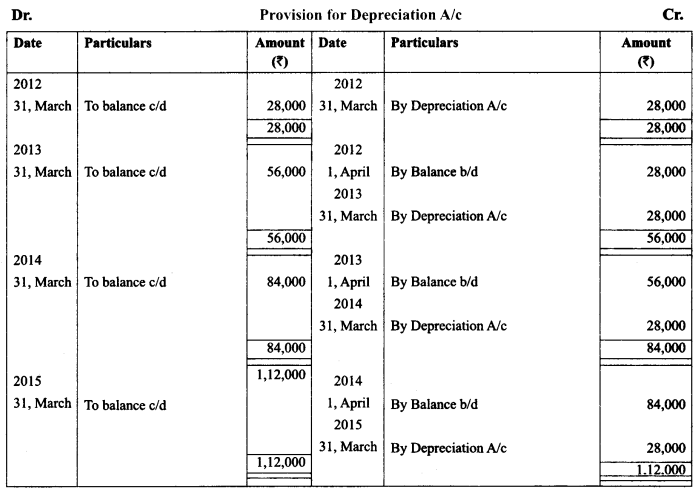

On April 01, 2011, Bajrang Marbles purchased a Machine for ₹ 2,80,000 and spend ₹ 10,000 on its carriage and ₹ 10,000 on its installation. It is estimated that its working life is 10 years and after 10 years its scrap value will be ₹ 20,000.

(a) Prepare Machine account and Depreciation account for the first four years by providing depreciation on straight line method. Accounts are closed on March 31st every year.

(b) Prepare Machine account, Depreciation account and Provision for depreciation account (or accumulated depreciation account) for the first four years by providing depreciation using straight line method. Accounts are closed on March 31 every year.

Solution:

(a)

Question 2.

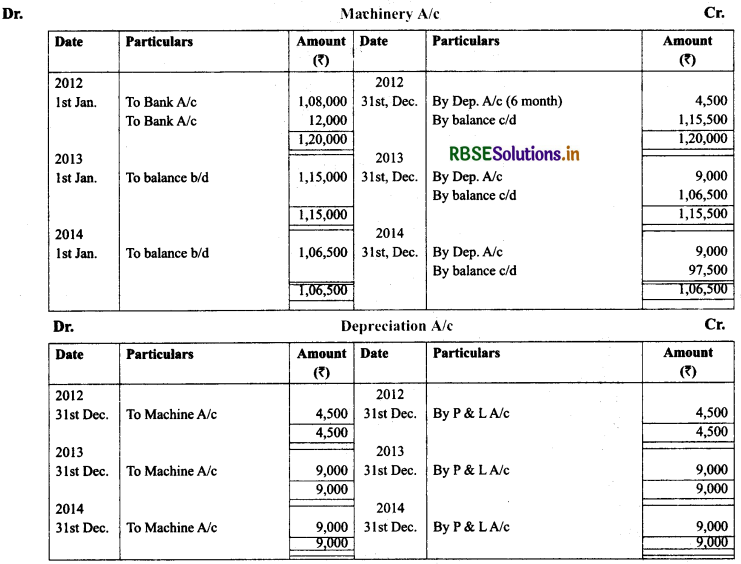

On July 01, 2012. Ashok Ltd. purchased a Machine for 1,08,000 and spent 12,000 on its installation. At the time of purchase it was estimated that the effective commercial life of the machine will be 12 years and after 12 years its salvage value will be 12,000. Prepare machine account and depreciation account in the books of Ashok Ltd. For first three years, if depreciation is written off according to straight line method. The account are closed on December 31st; every year.

Solution:

Question 3.

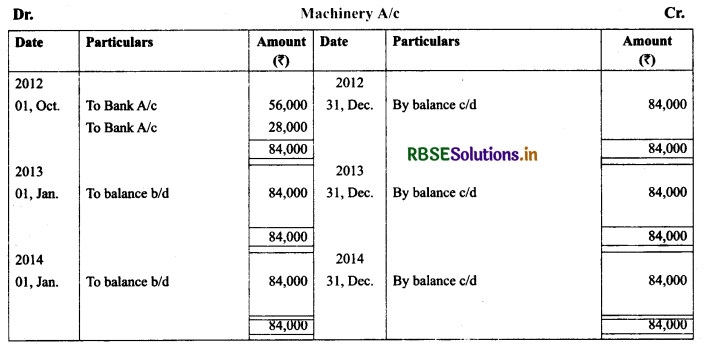

Reliance Ltd. Purchased a second hand machine for ₹ 56,000 on October 01, 2012 and spent ₹ 28,000 on its overhaul and installation before putting it to operation. It is expected that the machine can be sold for ₹ 6,000 at the end of its useful life of 15 years. Moreover an estimated cost of ₹ 1,000 is expected to be incurred to recover the salvage value of ₹ 6,000. Prepare machine account and Provision for depreciation account for the first three years charging depreciation by fixed installment method. Accounts are closed on December 31, every year.

Solution:

Question 4.

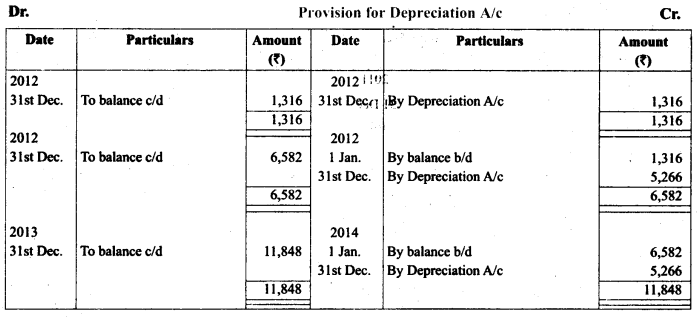

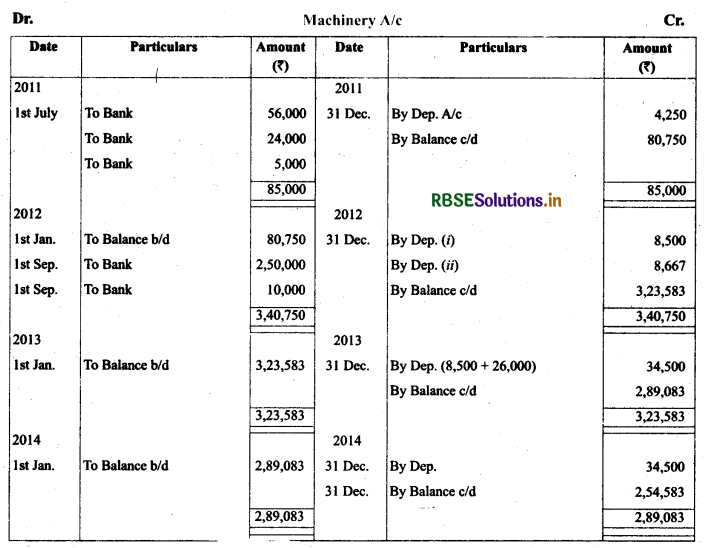

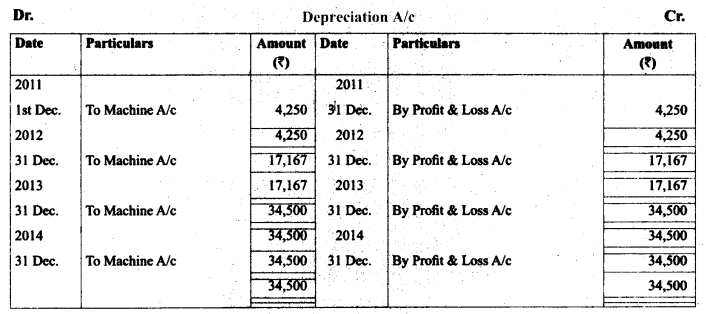

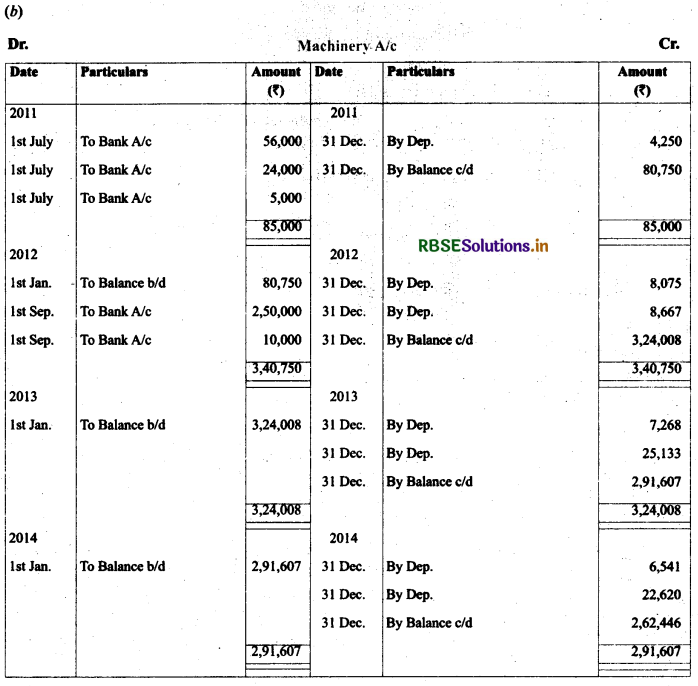

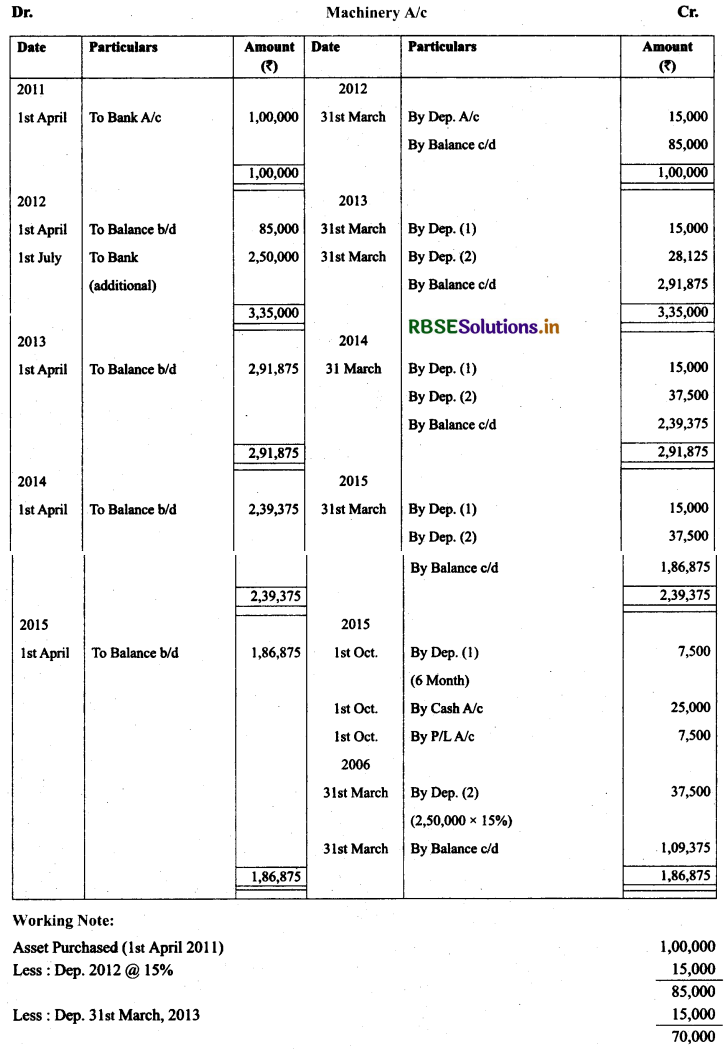

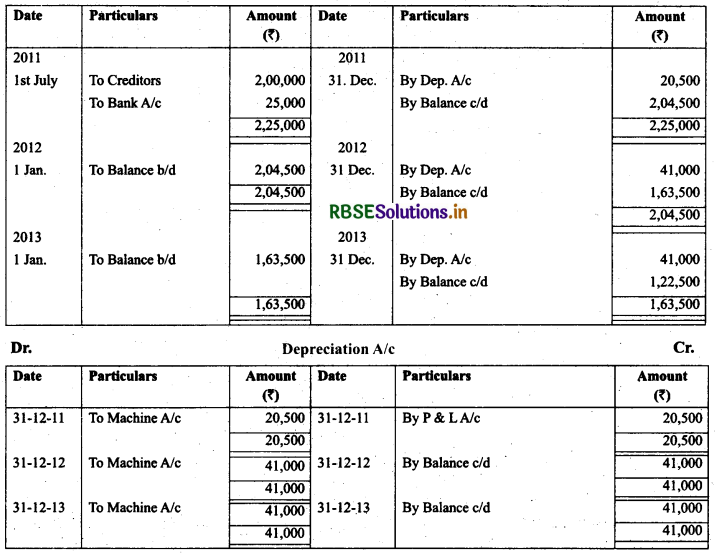

Berlia Ltd. purchased a second hand machine for ₹ 56,000 on July 01, 2011 and spent ₹ 24,000 on its repair and installation and ₹ 5,000 for its carriage. On September 01,2012, it purchased another machine for ₹ 2,50,000 and spent ₹ 10,000 on its installation.

(a) Depreciation is provided on machinery @10% p.a. on original cost method annually on December 31. Prepare machinery account and depreciation account from the year 2011 to 2014.

(b) Prepare machinery account and depreciation account from the year 2011 to 2014, if depreciation is provided on machinery @ 10% p.a. on written down value method annually on December 31.

Solution: (a)

Question 5.

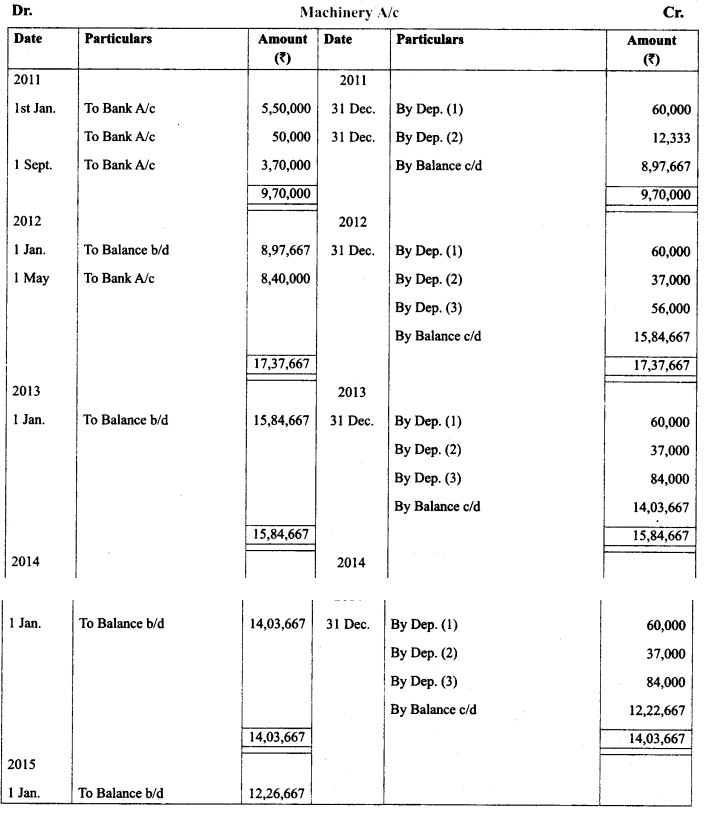

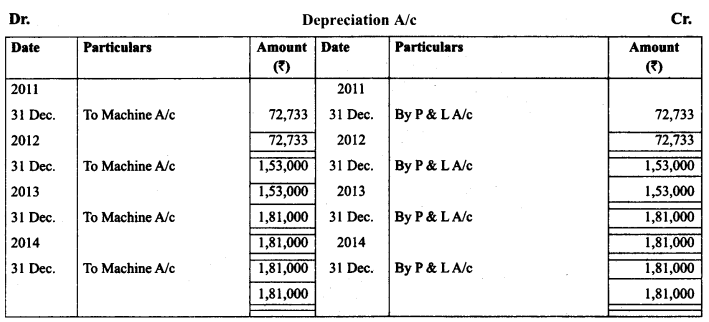

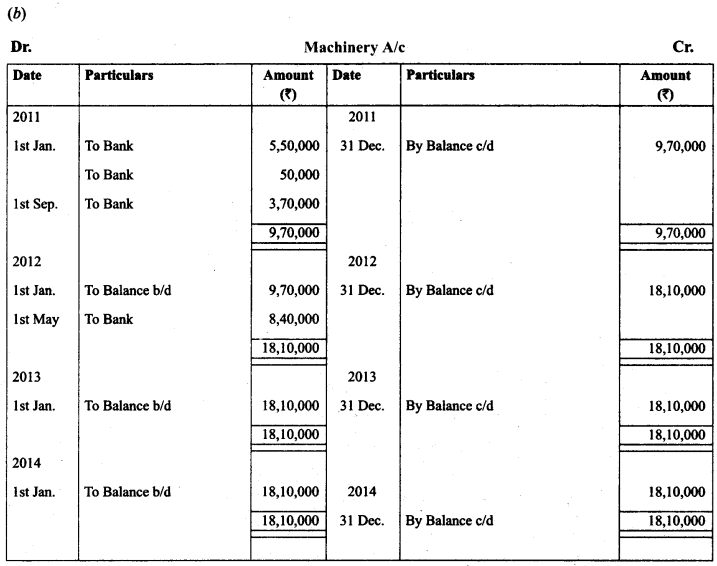

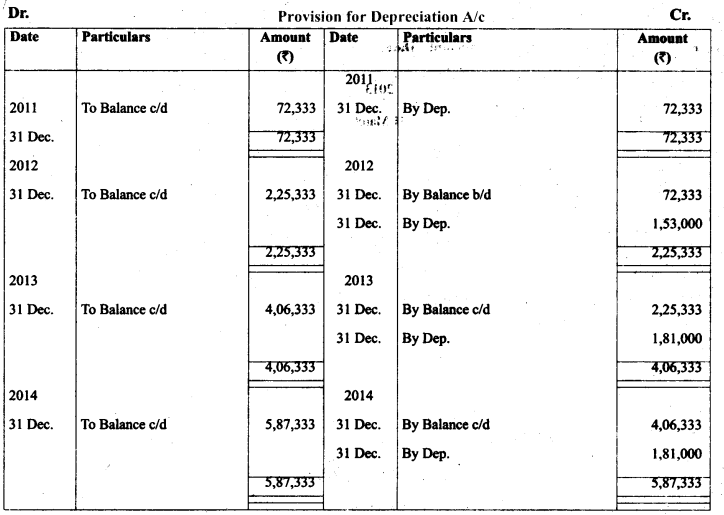

Ganga Ltd. purchased a machinery on January 01. 2011 for ₹ 5,50,000 and spent ₹ 50,000 on its installation. On September 01, 2011 it purchased another machine for ₹ 3,70,000. On May 01, 2012 it purchased another machine for ₹ 8,40,000 (including installation expenses.)

Depreciation was provided on machinery @ 10% p.a. on original cost method annually on December 31. Prepare:

(a) Machinery account and depreciation account for the years 2011, 2012,2013 and 2014.

(b) If depreciation is accumulated in the provision for Depreciation account then prepare machine account and provision for depreciation account for the years 2001,2002,2003 and 2004.

Solution:

Working Notes:

(1) 1 Jan. 2011 Machinery purchased (550,000 + 50,000) 6,00,000

Depreciation = 600,000 @ 10% = 60,000

(2) 1 Sept. 2011 Machinery purchased = 3,70,000 for 10% for 4 Months

Depreciation = 3,70,000 ( 10% for 4 months = 12,333)

Question 6.

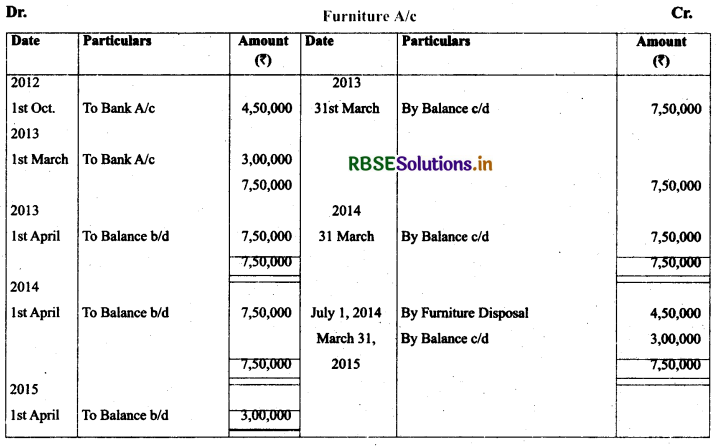

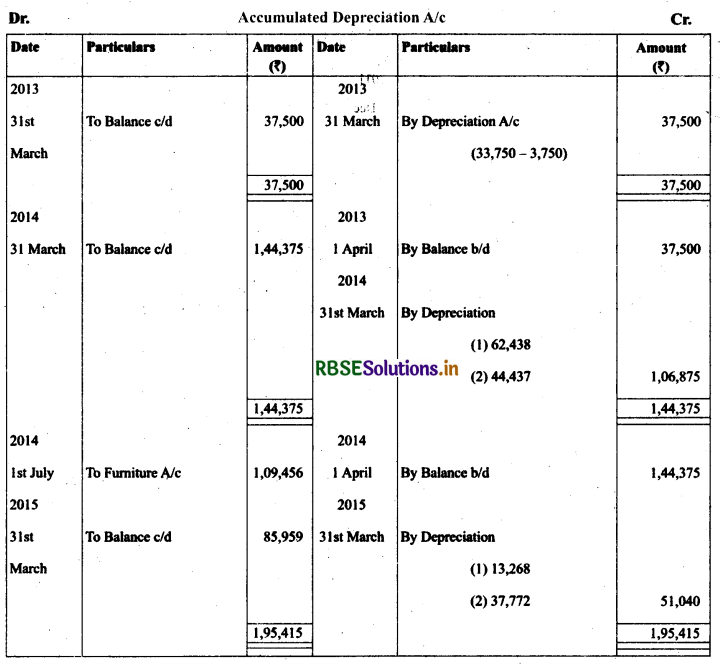

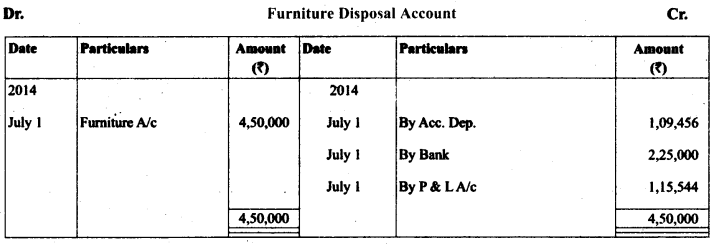

Azad Ltd. purchased furniture on October 01,2012 for ₹ 4,50,000. On March 01,2013 it purchased another furniture for ₹ 3,00,000. On July 01,2014 it sold off the first furniture purchased in 2012 for ₹ 2,25,000. Depreciation is provided at 15% p.a. on written down value method each year. Accounts are closed each year on March 31. Prepare furniture account and accumulated depreciation account for the years ended on March 31.2013. March 31,2014 and March 31, 2015. Also give the above two accounts if furniture disposal account is opened.

Solution:

Question 7.

M/s Lokesh Fabrics purchased a Taxtile Machine on April 01,2011 for ₹ 1,00,000. On July 01,2012 another machine costing ₹ 2,50,000 was purchased. The machine purchased on April 01,2011 was sold for ₹ 25,000 on October 01,2015. The company charges depreciation @15% p.a. on straight line method. Prepare machinery account and machinery disposal account for the year ended March 31,2016.

Solution:

Question 8.

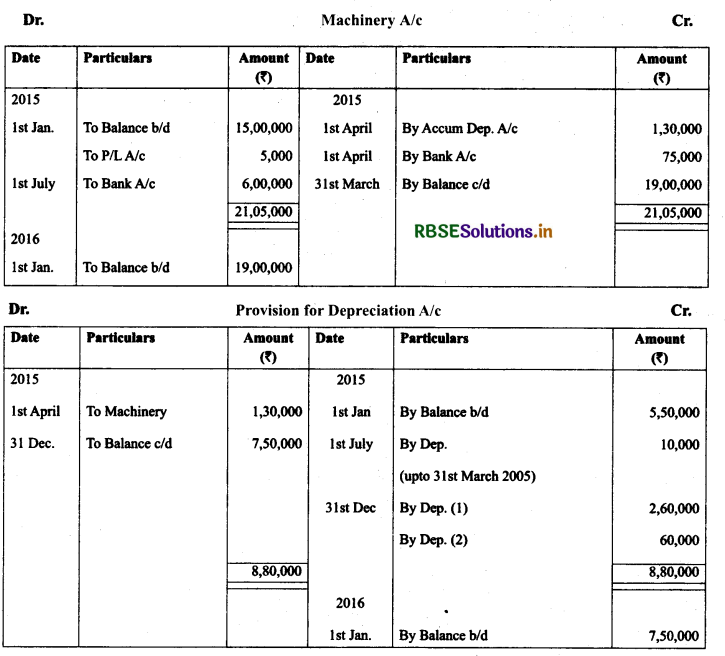

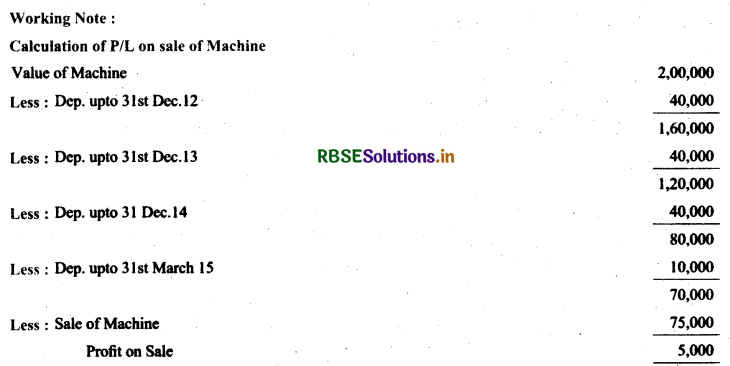

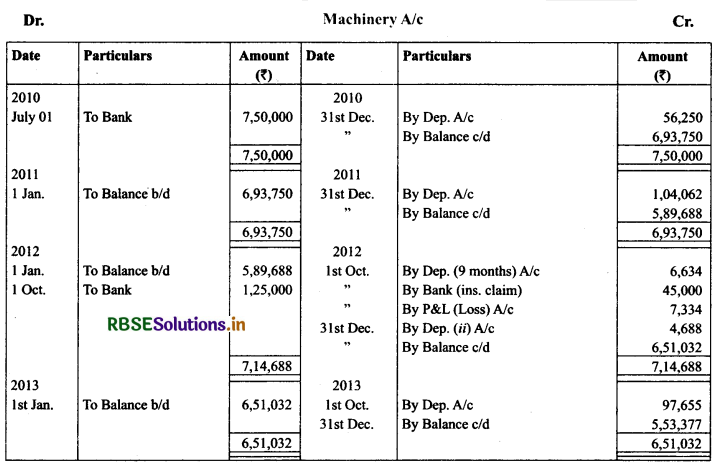

The following balances appear in the books of Crystal Ltd. on Jan. 01,2015 Machinery account ₹ 15,00,000 Provision for depreciation account ₹ 5,50,000 On April 01, 2015 a machinery which was purchased on January 01, 2012 for ₹ 2,00,000 was sold for ₹ 75,000. A new machine was purchased on July 01, 2015 for ₹ 6,00,000. Depreciation is provided on machinery at 20% p.a. on Straight line method and books are closed on December 31 every year. Prepare the machinery account and provision for depreciation account for the year ending December 31, 2015.

Solution:

Question 9.

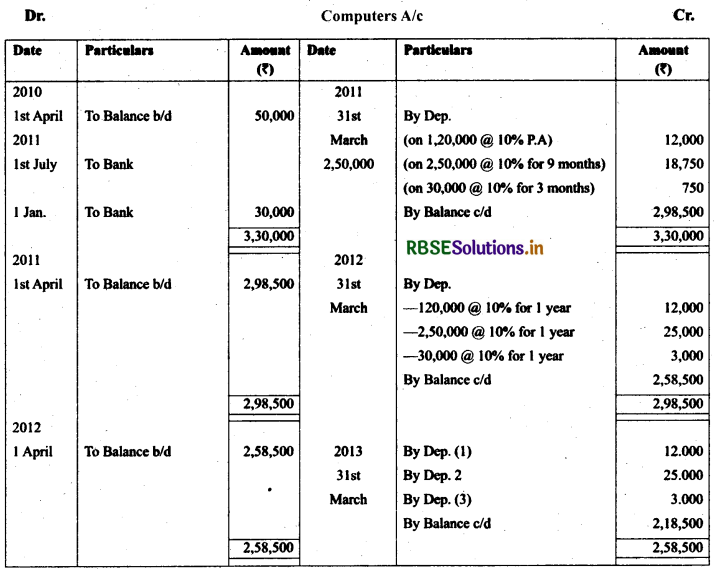

M/s. Excel Computers has a debit balance of ₹ 50,000 (original cost ₹ 1,20,000) in computers account on April 01, 2010. On July 01, 2010 it purchased another computer costing ₹ 2,50,000. One more computer was purchased on January 01,2011 for ₹ 30,000. On April 01,2014 the computer which was purchased on July 01,2010 became obselete and was sold for ₹ 20,000. A new version of the IBM computer was purchased on August 01,2014 for ₹ 80,000. Show Computers account in the books of Excel Computers for the years ended on March 31, 2011, 2012, 2013, 2014 and 2015. The computer is depreciated @ 10 p.a. on straight line method basis.

Solution.

* The balance of first computer as on 1.04.04 is ₹ 20,000, so the depreciation charged on it is only ₹ 2000.

* Loss on sale of computer = 2,50,000 - 18,750 - 25,000 - 25,000 - 25,000 - 20,000.

* Charged depreciation on third computer for 8 months.

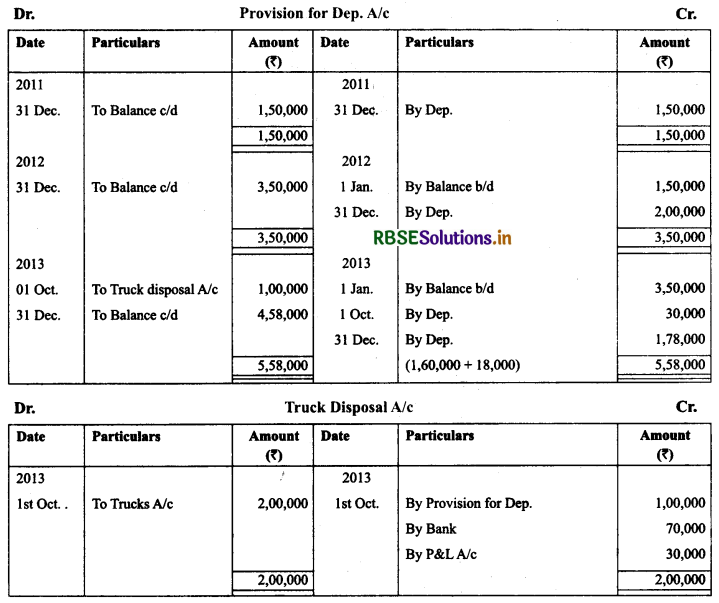

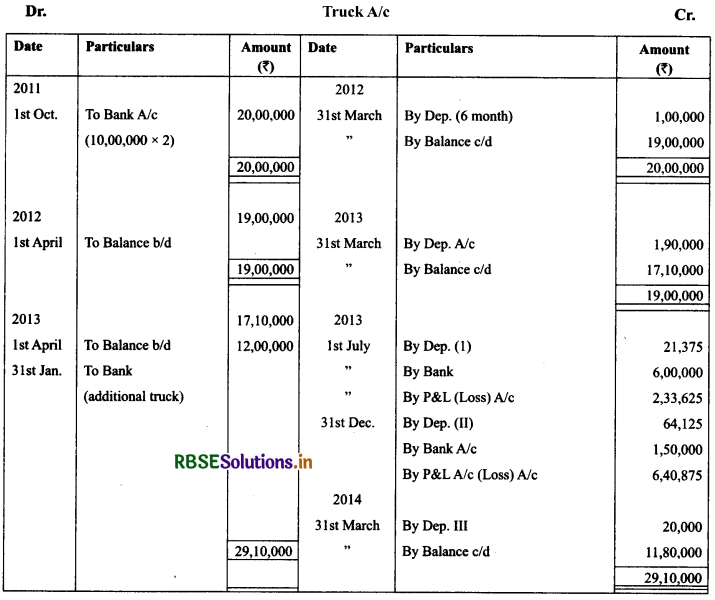

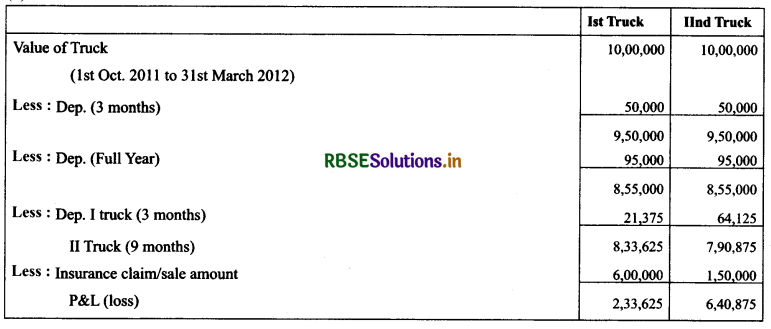

Question 10.

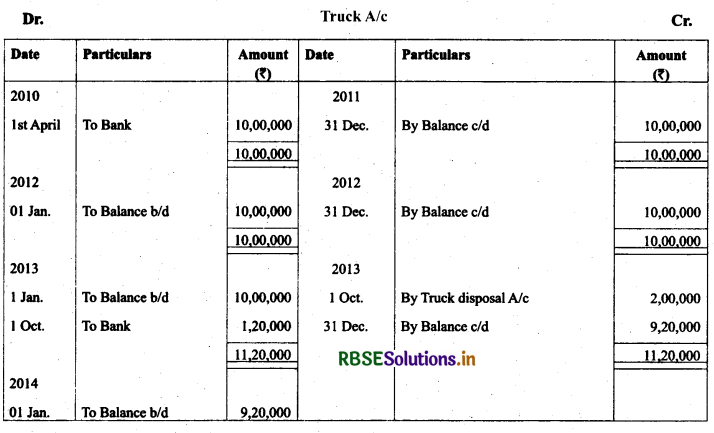

Carriage Transport Company purchased 5 trucks at the cost of₹ 2,00,000 each on April 01, 2011. The company writes off depreciation @ 20% p.a. on original cost and closes its books on December 31, every year. On October 01, 2013 one of the trucks is involved in an accident and is completely destroyed. Insurance company has agreed to pay ₹ 70,000 in full settlement of the claim. On the same date the company purchased a second hand truck for ₹ 1,00,000 and spent ₹ 20,000 on its overhauling. Prepare truck account and provision for depreciation account for the three years ended on December 31,2013. Also give truck account if truck disposal account is prepared.

Solution:

Question 11.

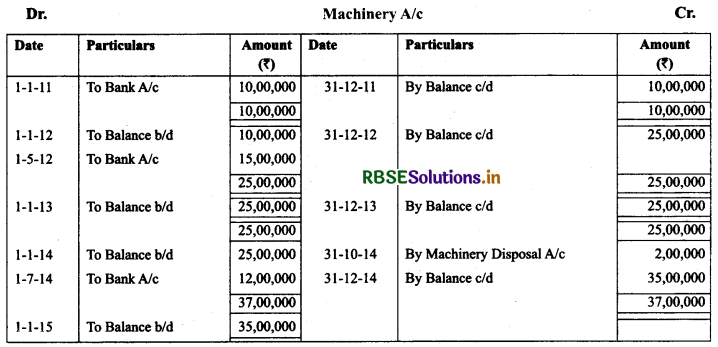

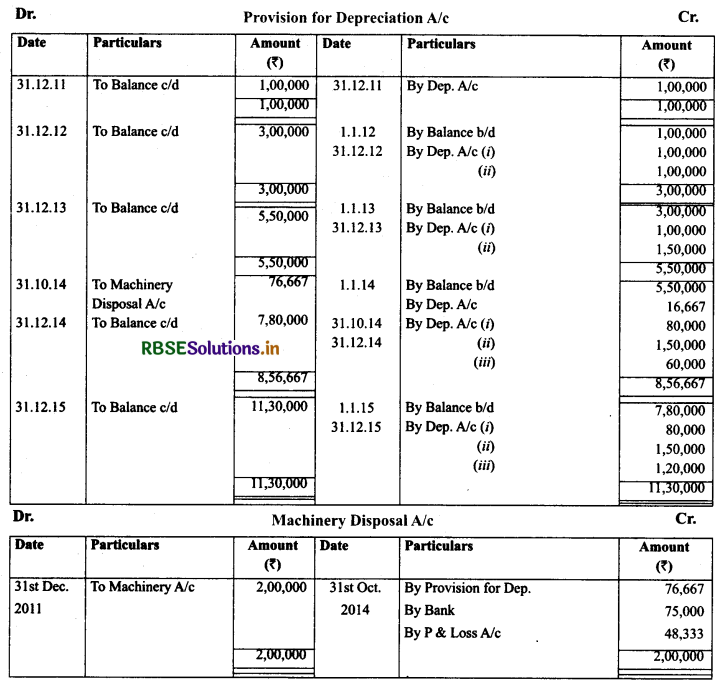

Saraswati Ltd. purchased a machinery costing ₹ 10,00,000 on January 01, 2011. A new machinery was purchased on 01 May, 2012 for ₹ 15,00,000 and another on July 01, 2014 for ₹ 12,00,000. A part of the machinery whose original cost was ₹ 2,00,000 was sold in 2011 for ₹ 75,000 on October 31, 2014. Show the machinery account, provision for depreciation account and machinery disposal account from 2011 to 2015 if depreciation is provided at 10% p.a. on original cost and account are closed on December 31, every year.

Solutions:

Question 12.

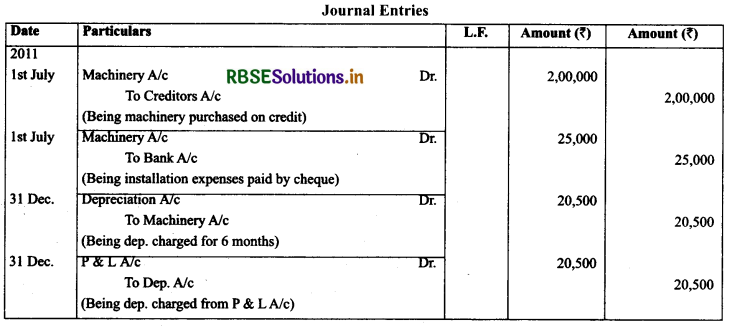

On July 01, 2011 Ashwani purchased a machine for ₹ 2,00,000 on credit. Installation expenses ₹ 25,000 are paid by cheque. The estimated life is 5 years and its scrap value after 5 years will be ₹ 20,000. Depreciation is to be charged on straight line basis. Show the journal entry for the year 2011 and prepare necessary ledger accounts for first three years.

Solution:

Question 13.

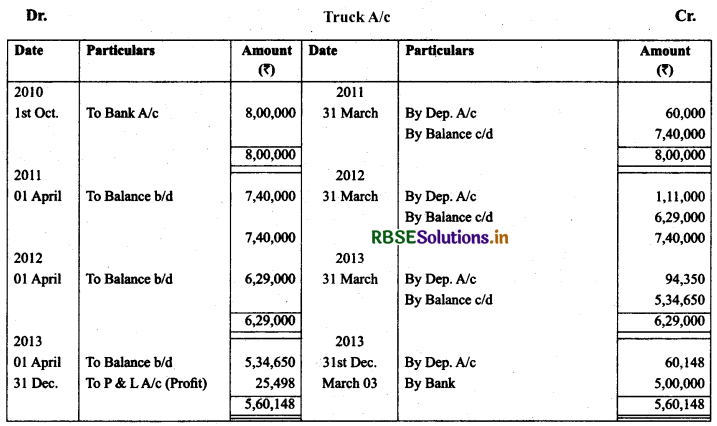

On October 01,2010 A truck was purchased for ₹ 8,00,000 by Laxmi Transport Ltd. Depreciation was provided at 15% p.a. on the diminishing balance basis on this truck. On December 31,2013 this Truck was sold for ₹ 5,00,000. Accounts are closed on 31st March every year. Prepare a Truck Account for the four years.

Solution:

Question 14.

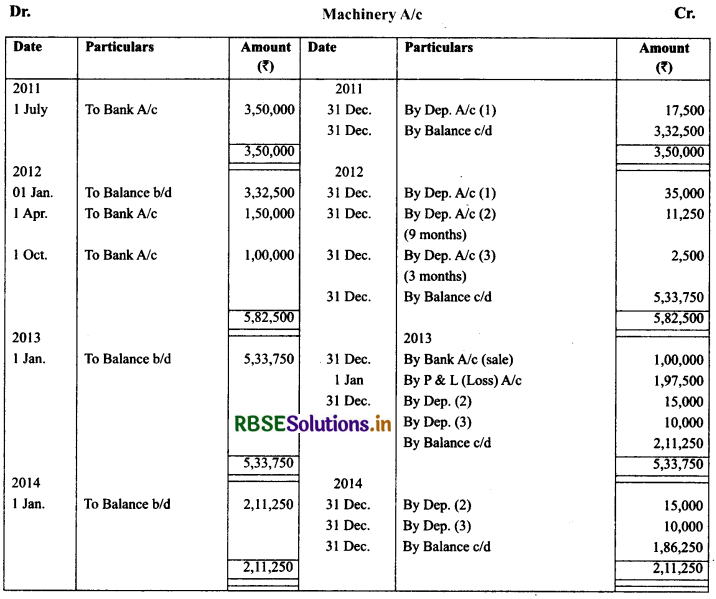

Kapil Ltd. purchased a machinery on July 01, 2011 for ₹ 3,50,000. It purchased two additional machines, on April 01, 2012 costing ₹ 1,50,000 and on October 01,2012 costing ₹ 1,00,000. Depreciation is provided @ 10% p.a. on straight line basis. On January 01,2013, first machinery become useless due to technical changes. This machinery was sold for ₹ 1,00,000 prepare machinery account for 4 years on the basis of calendar year.

Solution:

Question 15.

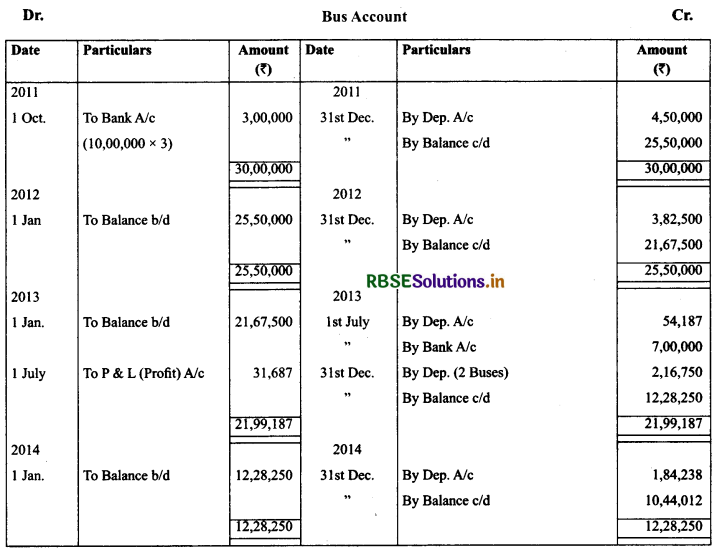

On January 01, 2011, Satkar Transport Ltd. purchased 3 buses for ₹ 10,00,000 each. On July 01, 2013, one bus was involved in an accident and was completely destroyed and ₹ 7,00,000 were received from the Insurance Company in full settlement. Depreciation is writen off @ 15% p.a. on diminishing balance method. Prepare bus account from 2011 to 2014. Books are closed on December 31 every year.

Solution:

Question 16.

On October 01,2011 Juneja Transport Company purchased 2 Trucks for ₹ 10,00,000 each. On July 01,2013, One Truck was involved in an accident and was completely destroyed and ₹ 6,00,000 were received from the insurance company in full settlement. On December 31, 2013 another truck was involved in an accident and destroyed partially, which was not insured. It was sold off for ₹ 1,50,000. On January 31,2014 company purchased a fresh truck for ₹ 12,00,000. Depreciation is to be provided at 10% p.a. on the written down value every year. The books are closed every year on March 31. Give the truck account from 2011 to 2014.

Working Note :

(1) Calculation of Profit & Loss on Sale of Trucks:

Question 17.

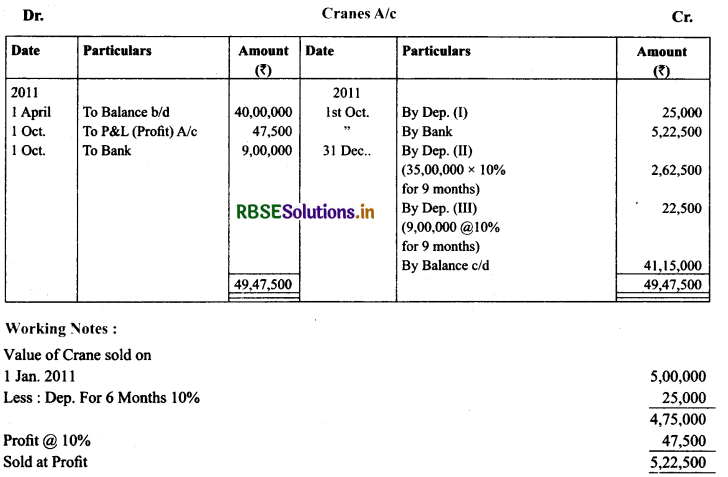

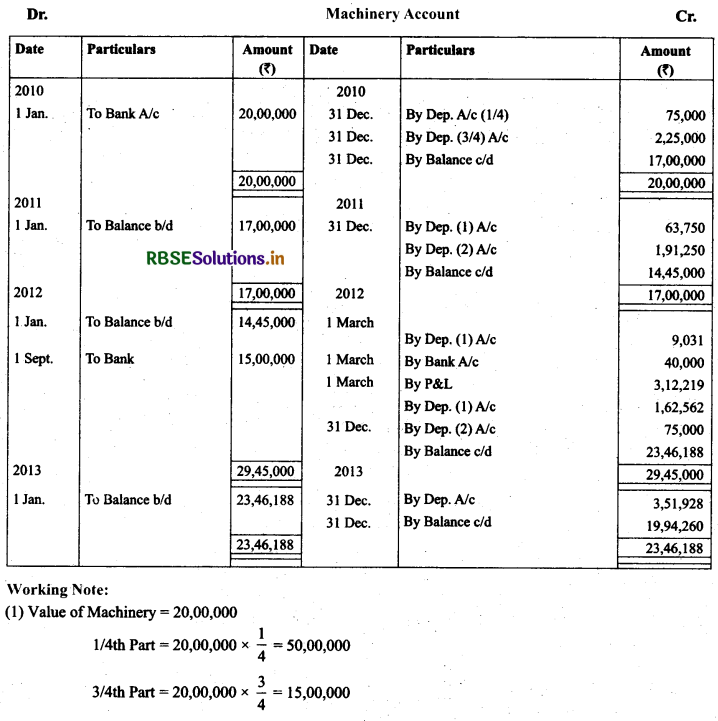

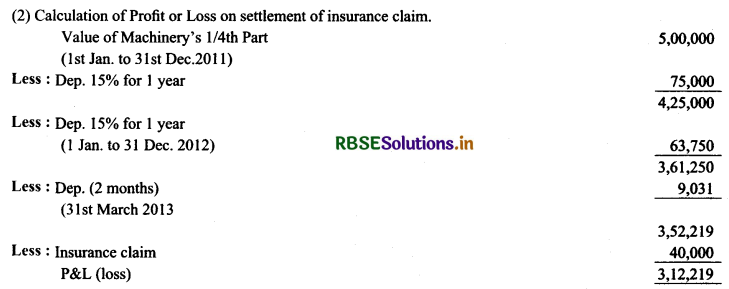

A Noida based Construction Company owns 5 cranes and the value of this asset in its books on April 01, 2011 is ₹ 40,00,000. On October 01,2011 it sold one of its cranes whose value was ₹ 5,00,000 on April 01,2011 at 10% profit. On the same day it purchased 2 cranes for ₹ 4,50,000 each. Prepare cranes account. It closes the books on December 31 and provides for depreciation on 10% written down value.

Solution:

Question 18.

Shri Krishan Manufacturing Company purchased 10 machines for ₹ 75,000 each on July 01,2010. On October 01,2012, one of the machines got destroyed by fire and an insurance claim of ₹ 45,000 was admitted by the company. On the same date another machine was purchased by the company for ₹ 1,25,000. The company writes off 15% p.a. depreciation on written down value basis. The company maintains the calendar year as its financial year. Prepare the machinery account from 2010 to 2013.

Solution.

Question 19.

On January 01,2010, a Limited Company purchased machinery for ₹ 20,00,000. Depreciation is provided @ 15% p.a. on diminishing balance method. On March 01, 2012, one fourth of machinery was damaged by fire and ₹ 40,000 were received from the insurance company in full settlement. On September 01, 2012 another machinery was purchased by the company for ₹ 15,00,000. Write up the machinery account from 2010 to 2013. Books are closed on December 31, every year.

Solution:

Question 20.

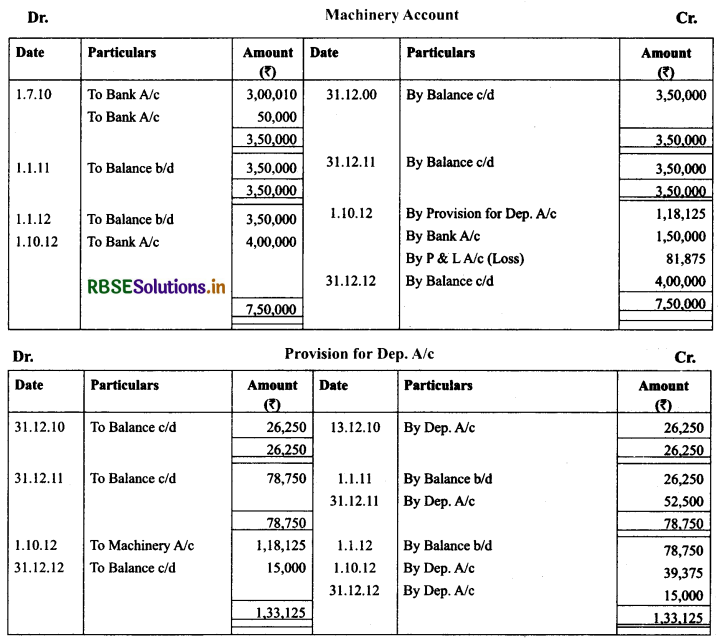

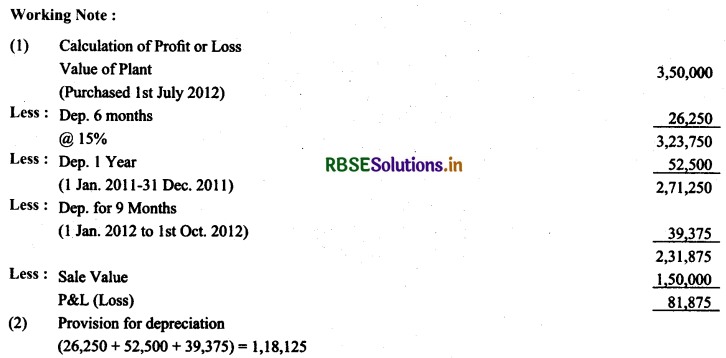

A Plant was purchased on 1st July, 2010 at a cost of₹ 3,00,000 and ₹ 50,000 were spent on its installation. The depreciation is written off at 15% p.a. on the straight line method. The plant was sold for ₹ 1,50,000 on October 01,2012 and on the same date a new Plant was installed at the cost of ₹ 4,00,000 including purchasing value. The accounts are closed on December 31 every year. Show the machinery account and provision for depreciation account for 3 years.

Solution:

Question 21.

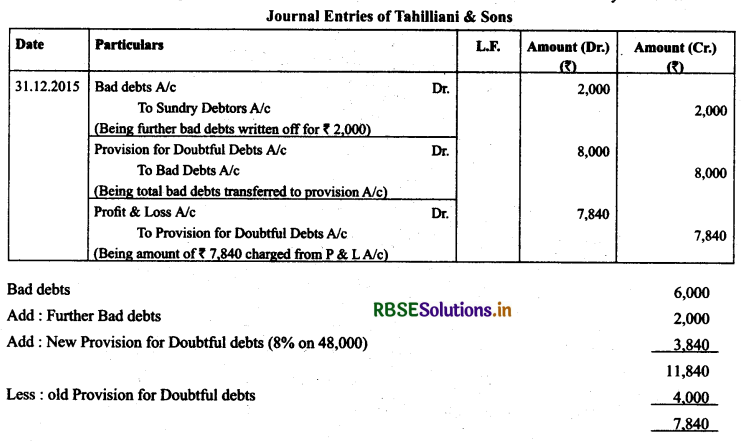

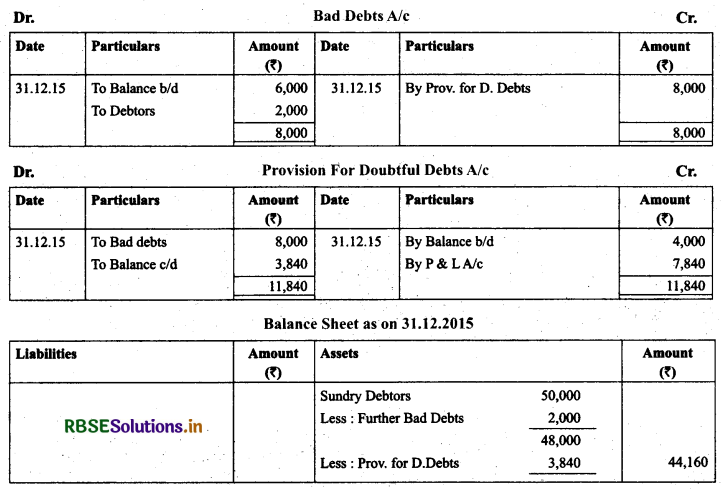

An extract of trial balance from the books of Tahilliani and sons enterprises on December 31,2015 is given below:

Additional Informations:

• Bad debts proved amounted to ₹ 2,000 but not recorded

• Provision is to be mainkined @ 8% of debtors

Make journal entries for provision for doubtful debts and bad debts write off. Make necessary accounts.

Solution:

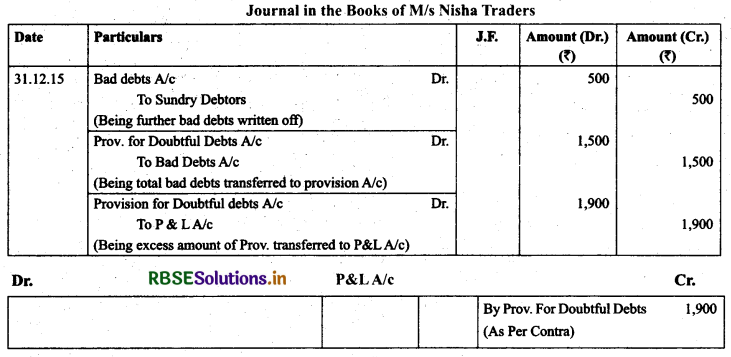

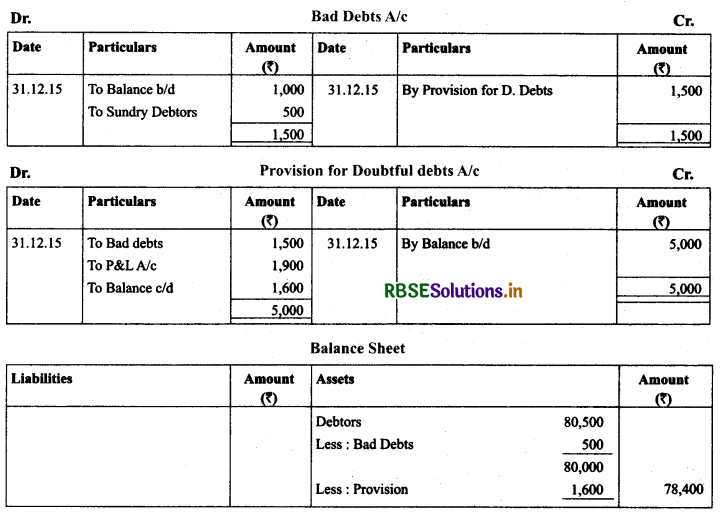

Question 22.

The following informations are extract from the Trial Balance of M/s Nisha Traders on 31 December, 2015 : Sundry Debtors

Solution.

- RBSE Solutions for Class 11 Accountancy Chapter 5 बैंक समाधान विवरण

- RBSE Solutions for Class 11 Accountancy Chapter 4 लेन-देनों का अभिलेखन-2

- RBSE Solutions for Class 11 Accountancy Chapter 6 तलपट एवं अशुद्धियों का शोधन

- RBSE Class 11 Accountancy Important Questions in Hindi & English Medium

- RBSE Solutions for Class 11 Economics Chapter 4 Presentation of Data

- RBSE Class 11 Accountancy Important Questions Chapter 12 Applications of Computers in Accounting

- RBSE Class 11 Accountancy Important Questions Chapter 11 Accounts from Incomplete Records

- RBSE Class 11 Accountancy Important Questions Chapter 10 Financial Statements-II

- RBSE Class 11 Accountancy Important Questions Chapter 9 Financial Statements-I

- RBSE Class 11 Accountancy Important Questions Chapter 7 Depreciation, Provisions and Reserves

- RBSE Class 11 Accountancy Important Questions Chapter 6 Trial Balance and Rectification of Errors